Three Graduate Projects Developed in Budgeting & Financial Management, AU:

Detroit Fiscal Transparency Budget Brief

Puerto Rico Budget Brief: A Growth-Friendly Path to Fiscal Sustainability

Flexible Budgeting and Cost Analysis: CentralCity Day Care

Puerto Rico Budget Brief: A Growth-Friendly Path to Fiscal Sustainability

Metrics

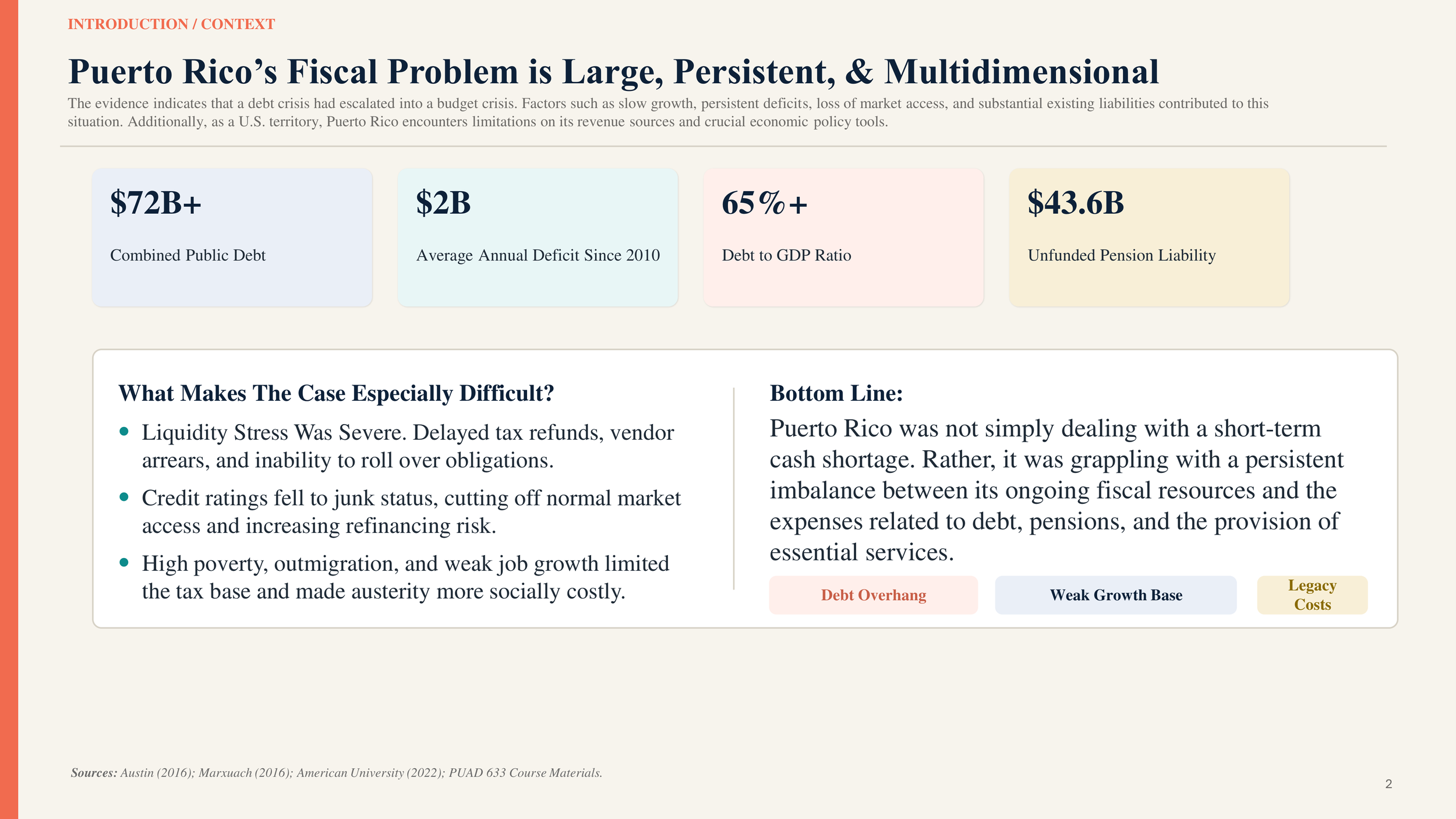

$72B+ Public Debt

Combined public debt burden.

$2B Annual Deficit

Average annual deficit since 2010.

65%+ Debt-to-GDP

A signal of fiscal overhang and limited flexibility.

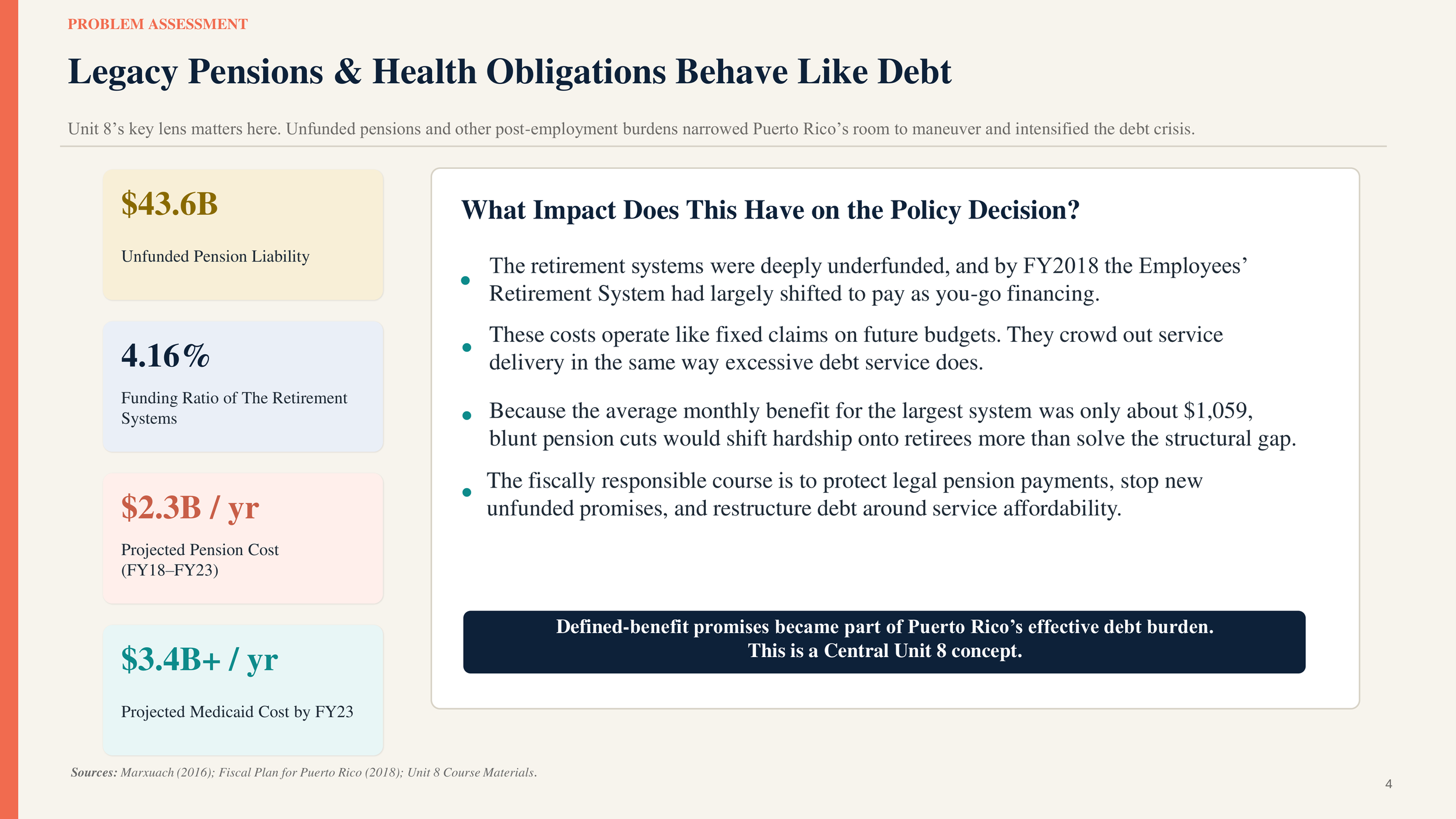

$43.6B Unfunded Pension Liability

Legacy liabilities operating like debt.

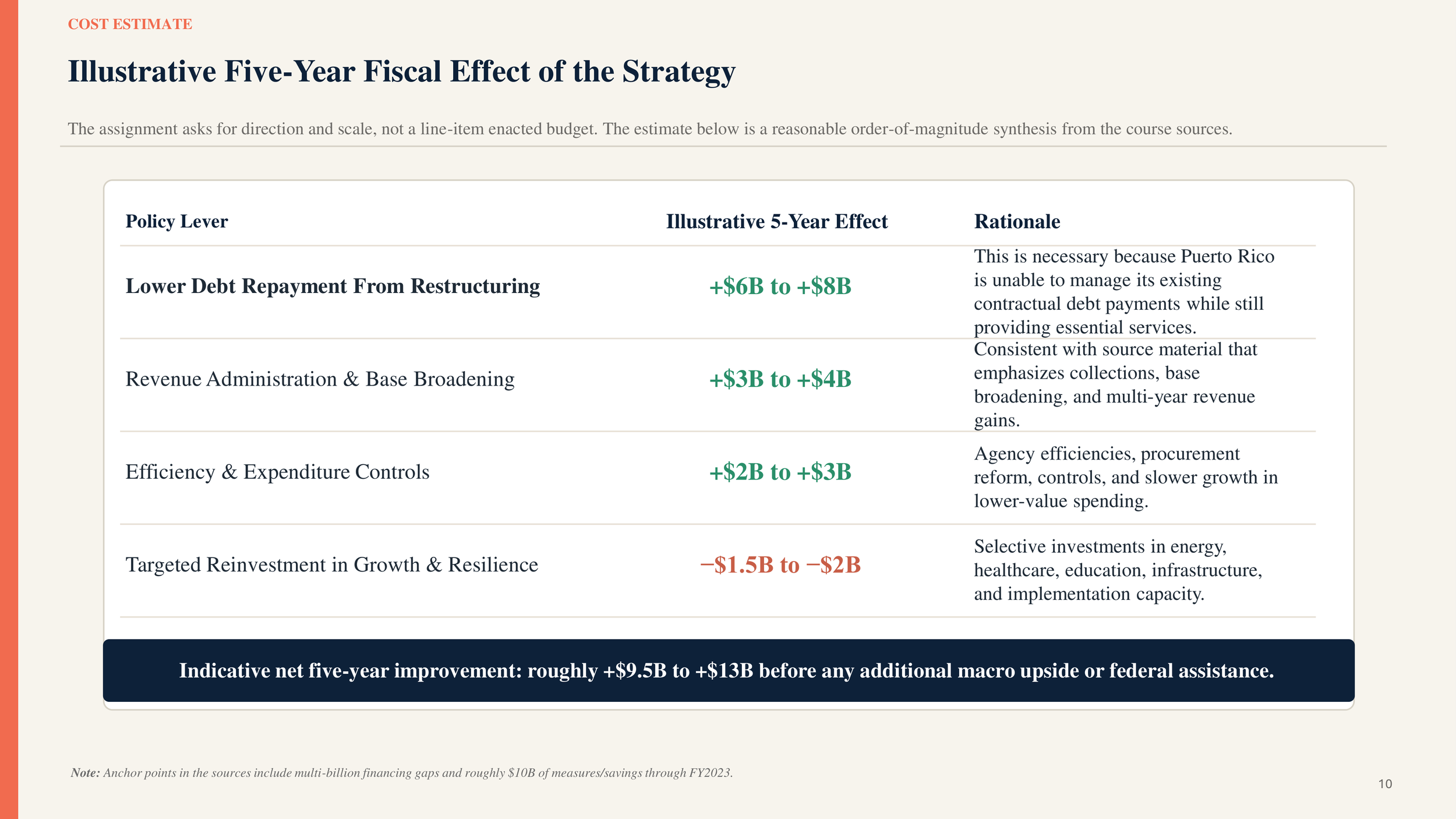

5-Year Net Improvement: +$9.5B to +$13B

Illustrative effect of the recommended package.

Overview

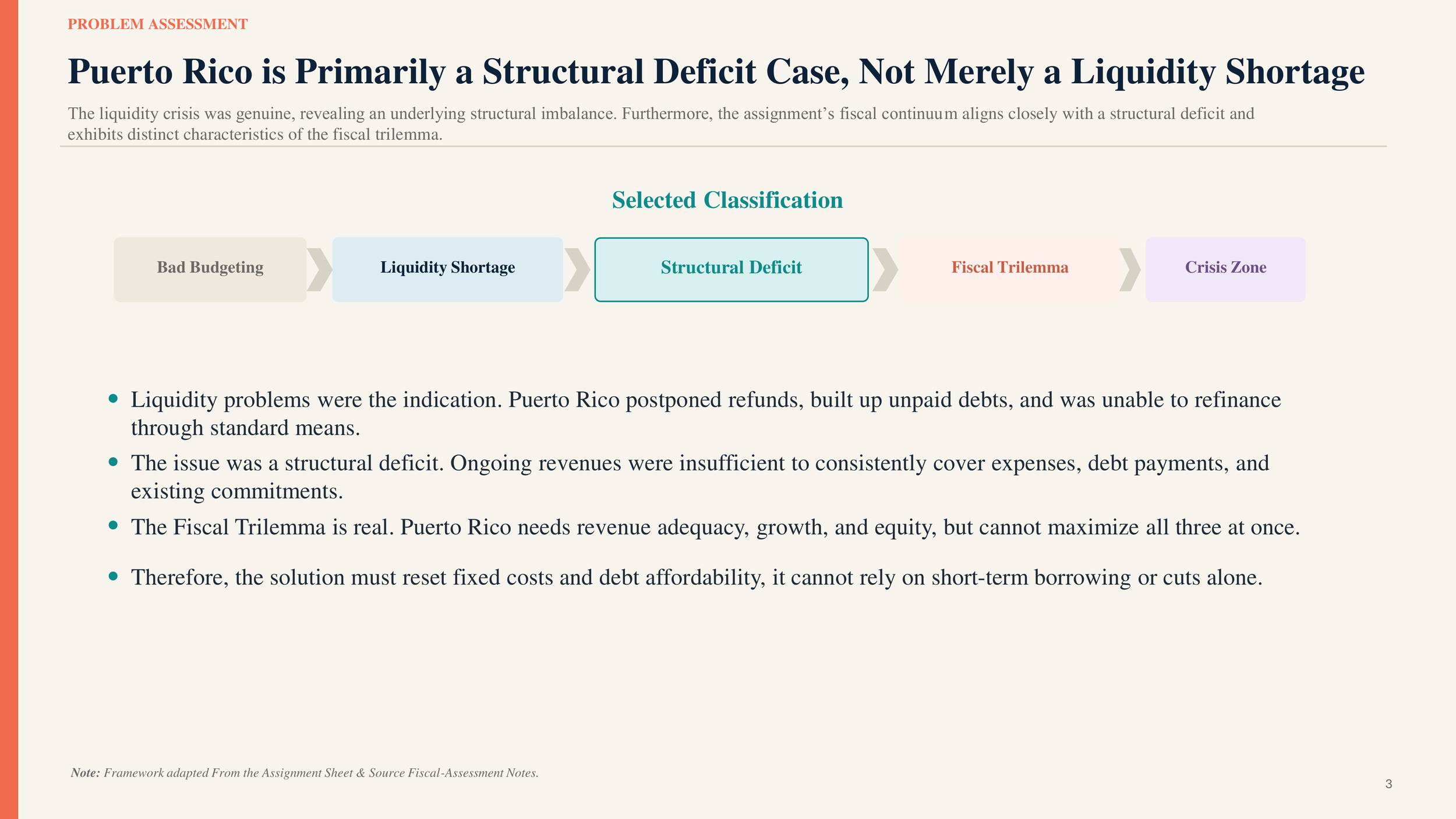

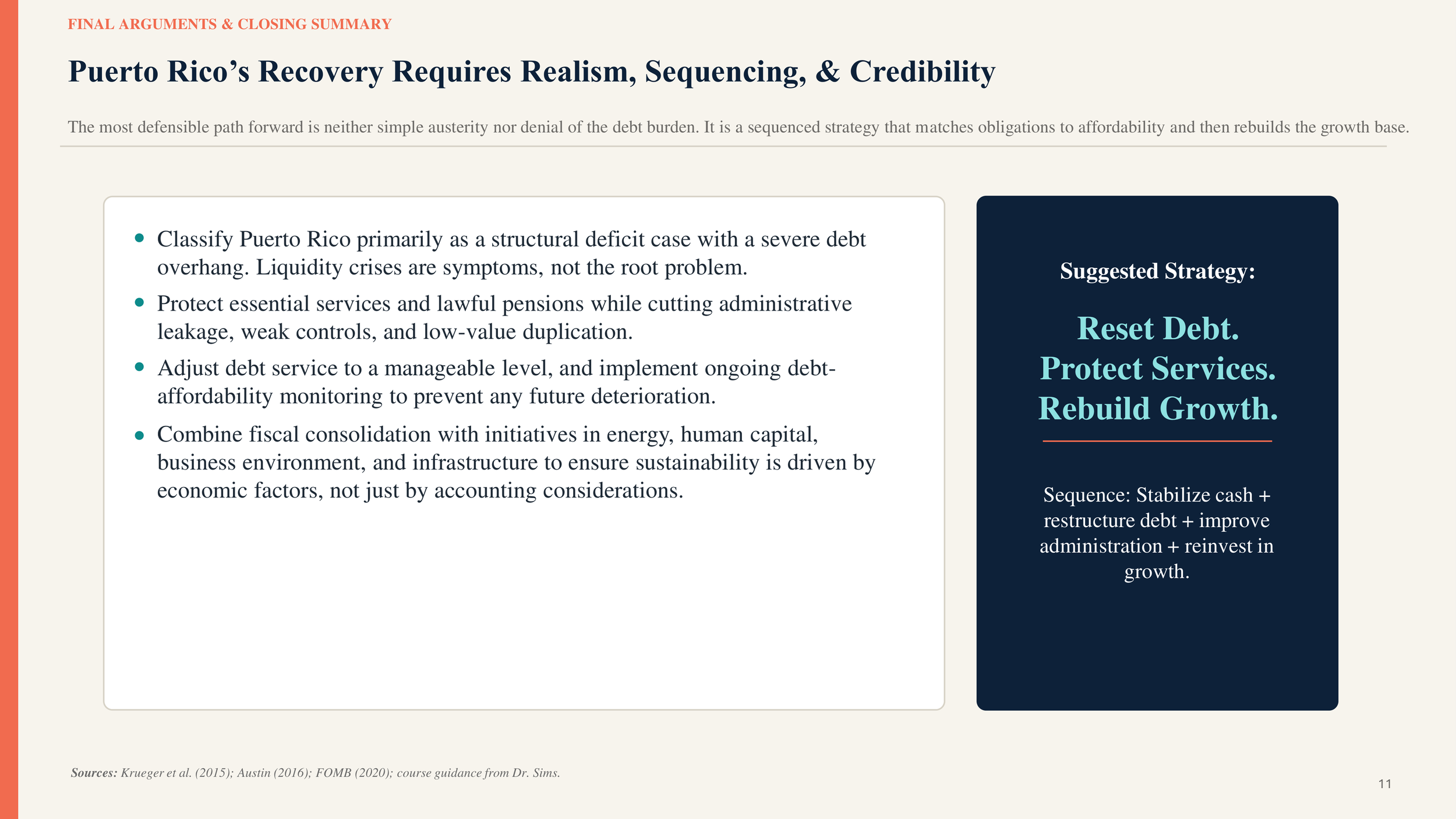

This project examined Puerto Rico’s fiscal crisis as more than a short-term liquidity shortage. The analysis classified Puerto Rico primarily as a structural deficit case with a severe debt overhang, shaped by slow growth, recurring deficits, limited market access, and substantial legacy liabilities. The goal was to identify a fiscally credible and growth-oriented path forward rather than a one-year balancing exercise.

What I Analyzed

The project evaluated Puerto Rico’s fiscal position through the lenses of:

Structural deficit versus liquidity shortage,

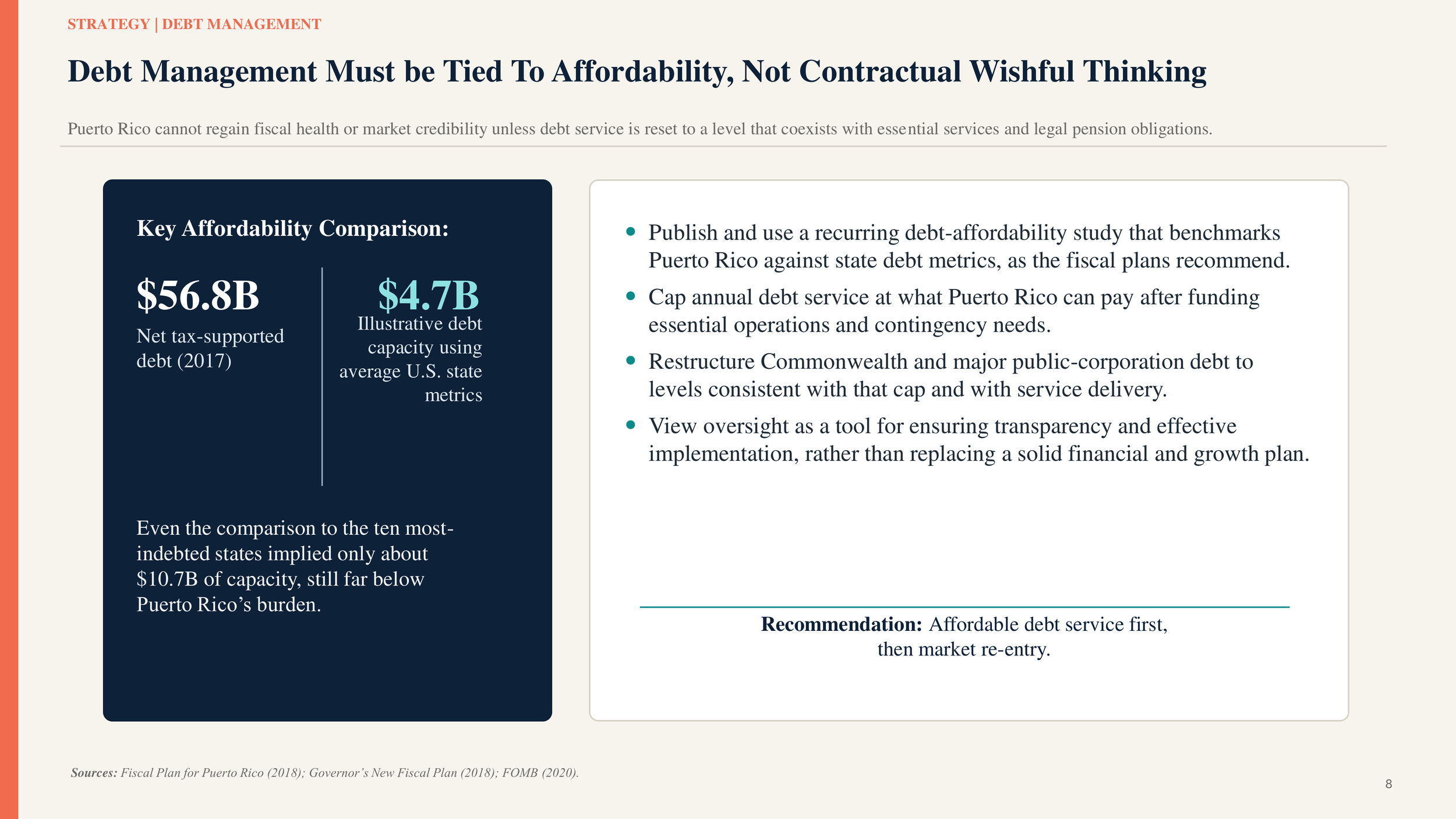

Debt affordability,

Unfunded pension and health obligations,

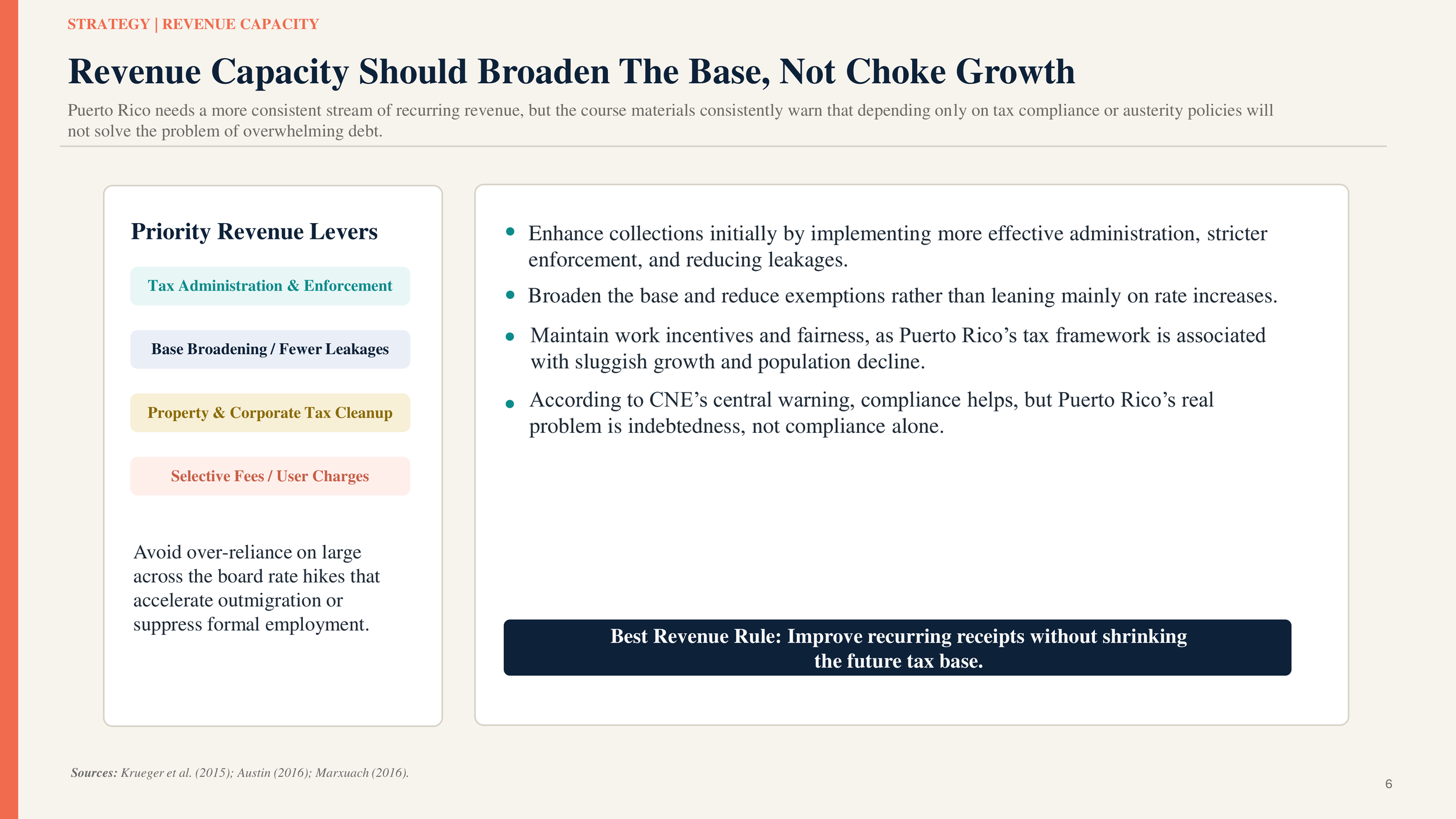

Revenue capacity,

Expenditure priorities,

Long-term growth potential.

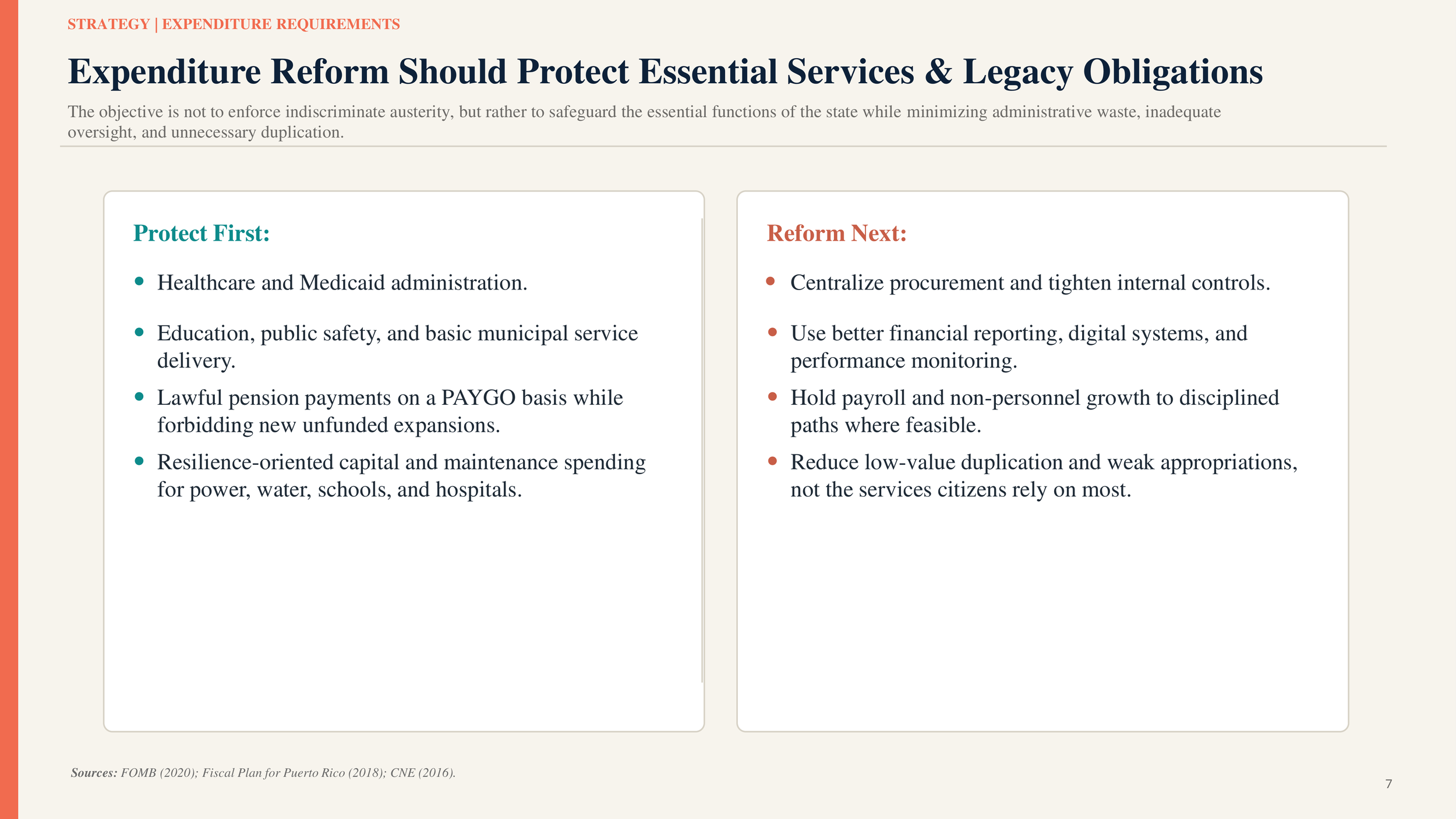

Note: The analysis emphasized that Puerto Rico’s challenge could not be solved through austerity or compliance measures alone. It required a strategy that matched obligations to affordability while protecting the state’s essential functions.

Key Fiscal Diagnosis

The brief argued that Puerto Rico’s crisis was fundamentally structural. Liquidity stress was real, but it reflected a deeper imbalance between recurring fiscal resources and the costs of debt service, pensions, healthcare, and essential public services. The project also applied the course’s fiscal-continuum concepts, positioning Puerto Rico in the zone of structural deficit and fiscal trilemma.

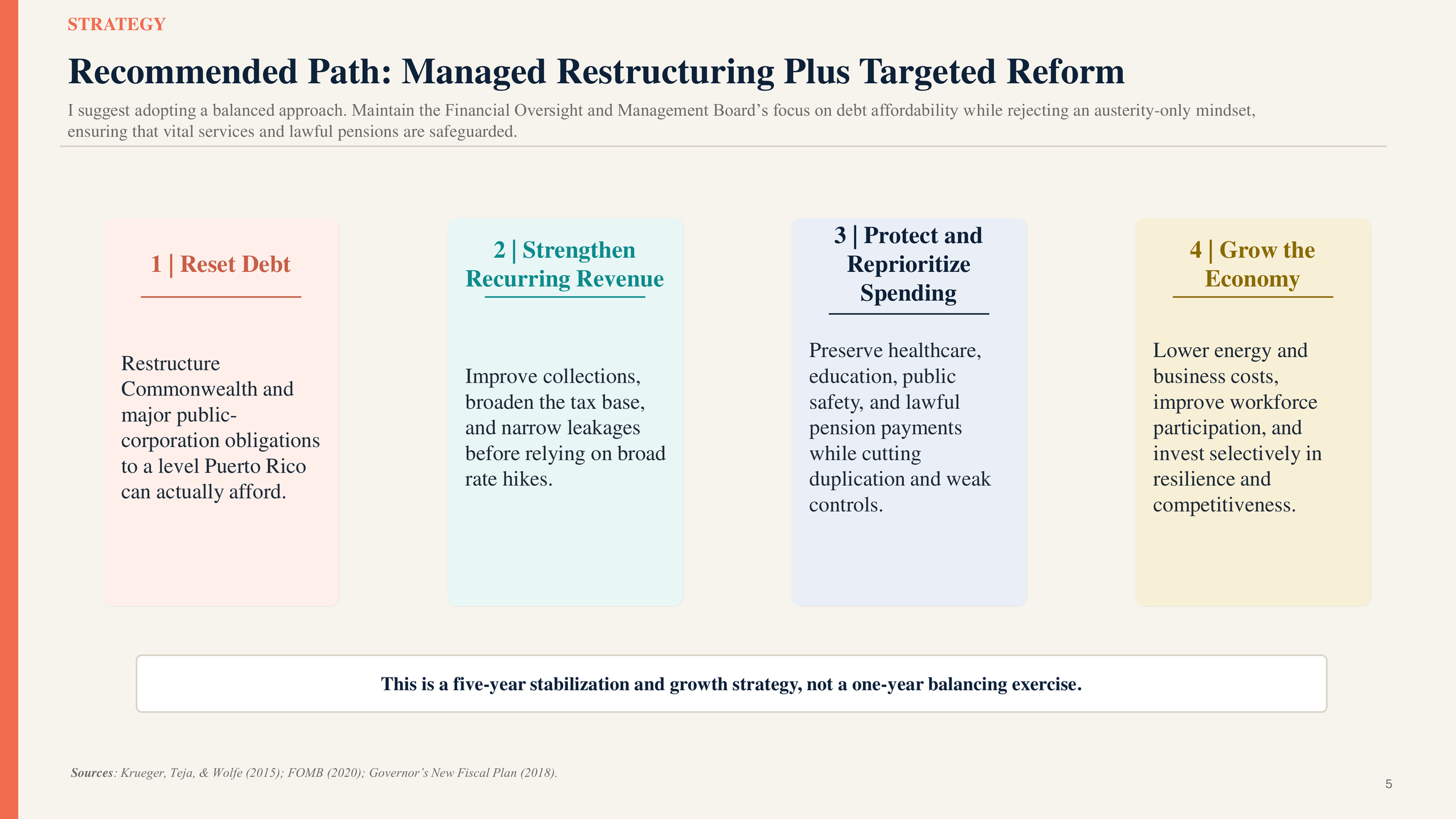

Recommended Strategy

The recommended path was a sequenced, growth-friendly package:

Reset debt to an affordable level

Strengthen recurring revenue through administration, enforcement, and base broadening

Protect and reprioritize spending around essential services and lawful pensions

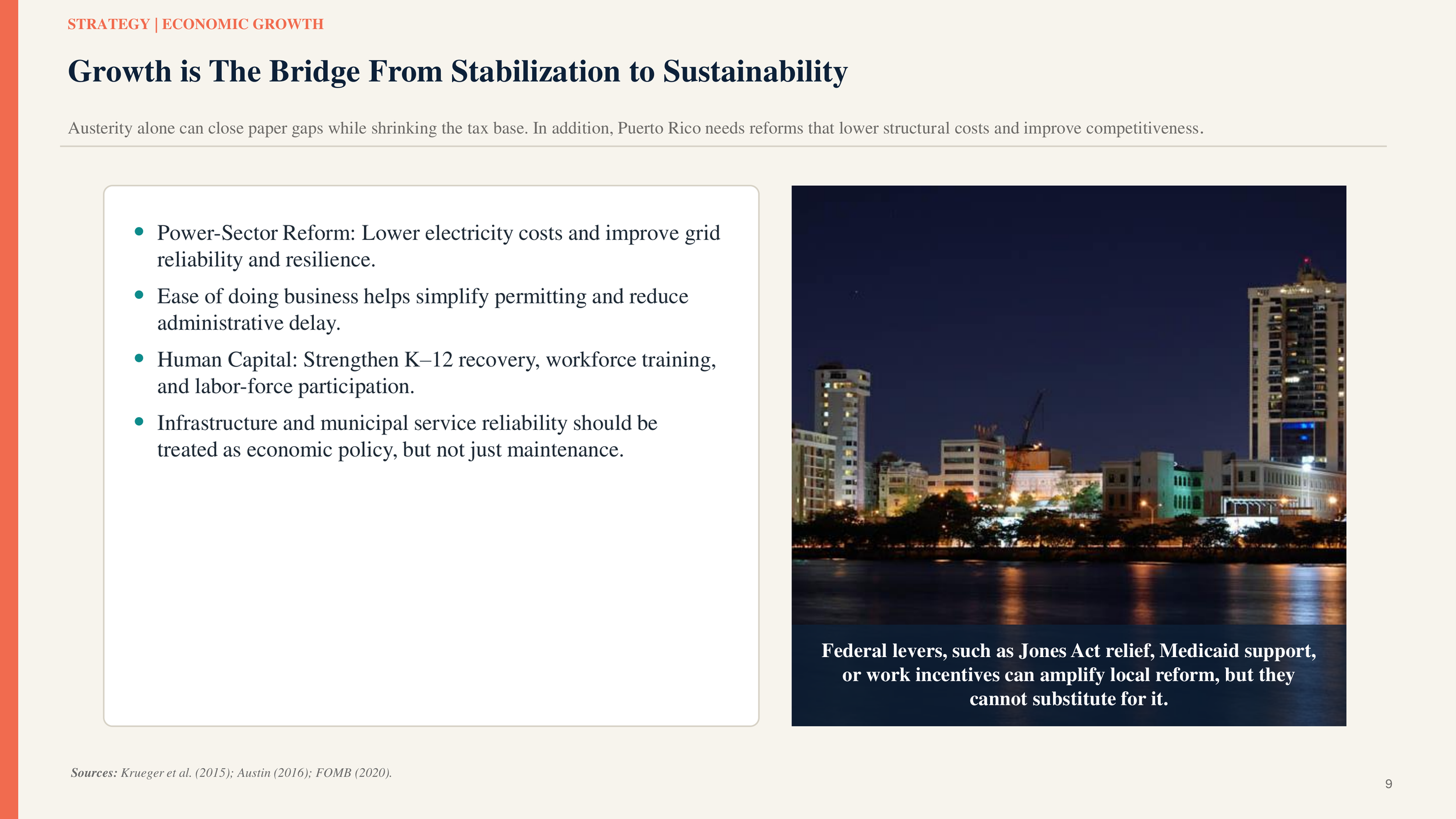

Support economic growth through competitiveness, infrastructure, and lower structural costs

Note: The brief explicitly rejected an austerity-only approach and instead argued for managed restructuring plus targeted reform.

Why It Matters

This project demonstrates the ability to analyze public financial distress in a structured and decision-oriented way. It shows skills in fiscal diagnosis, budget strategy, debt-affordability reasoning, expenditure prioritization, and the relationship between budgeting and long-term growth. It also reflects an important analytical discipline: distinguishing between short-term cash stress and deeper structural imbalance.

Professional Relevance

This work mirrors the kind of reasoning required in government, budgeting, fiscal policy, oversight, and public-finance roles. It connects budget choices to debt, pensions, service delivery, administrative controls, and economic competitiveness, showing the ability to think about public finance not only in accounting terms, but also in strategic and institutional terms.

Key Skills

Skills Demonstrated:

Fiscal analysis

Structural deficit assessment

Debt affordability analysis

Pension and legacy-cost interpretation

Budget strategy development

Public-sector prioritization

Cost-estimate reasoning

Professional budget writing

Personal Reflection

This project reflects my graduate training in budgeting and financial management and my interest in how public institutions can move from fiscal crisis toward sustainability through sequencing, realism, and credible long-term strategy.

Detroit Fiscal Transparency Budget Brief

Metrics

3 Fiscal Years Reviewed

FY2011–12 through FY2013–14.

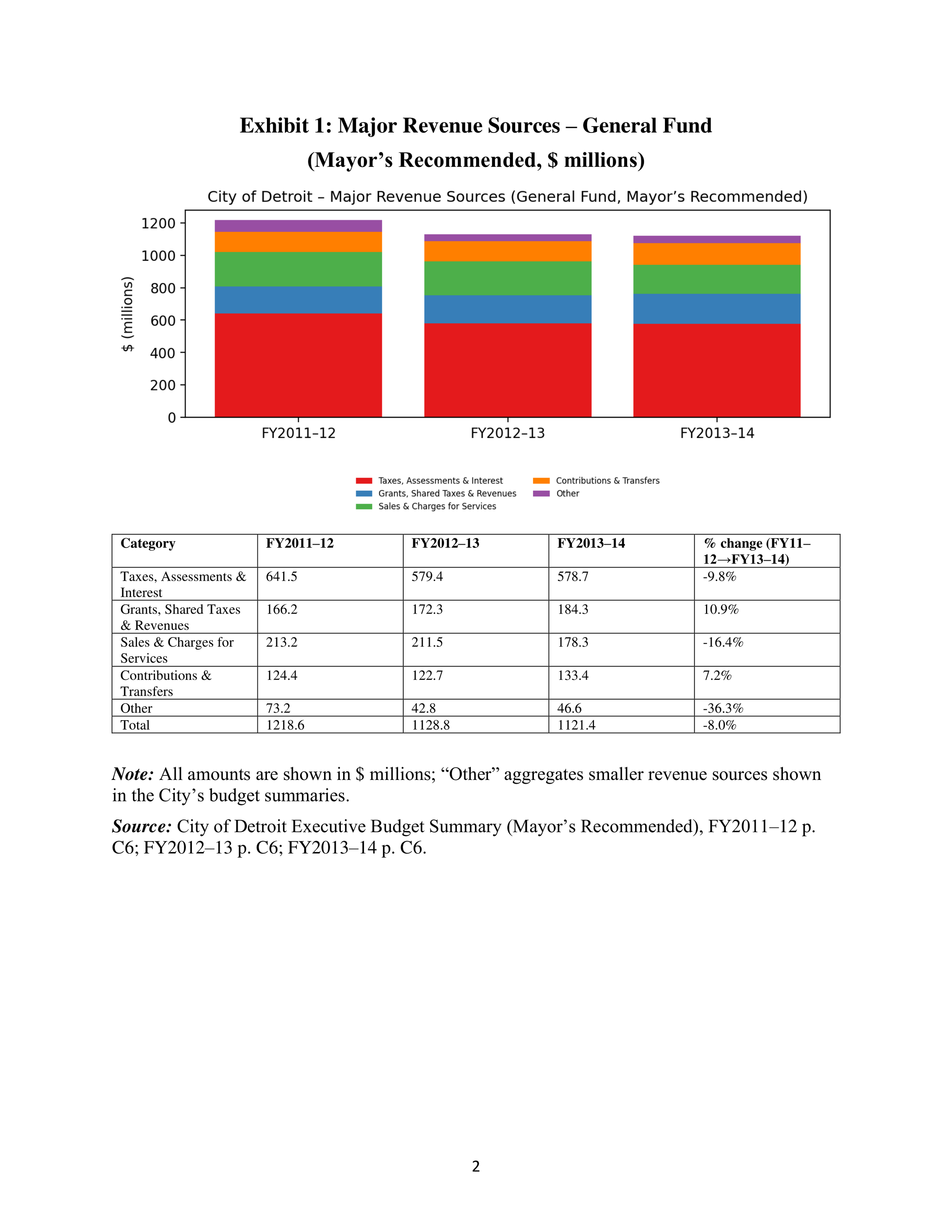

8% Revenue Decline

Major General Fund revenues fell from about $1.22B to $1.12B.

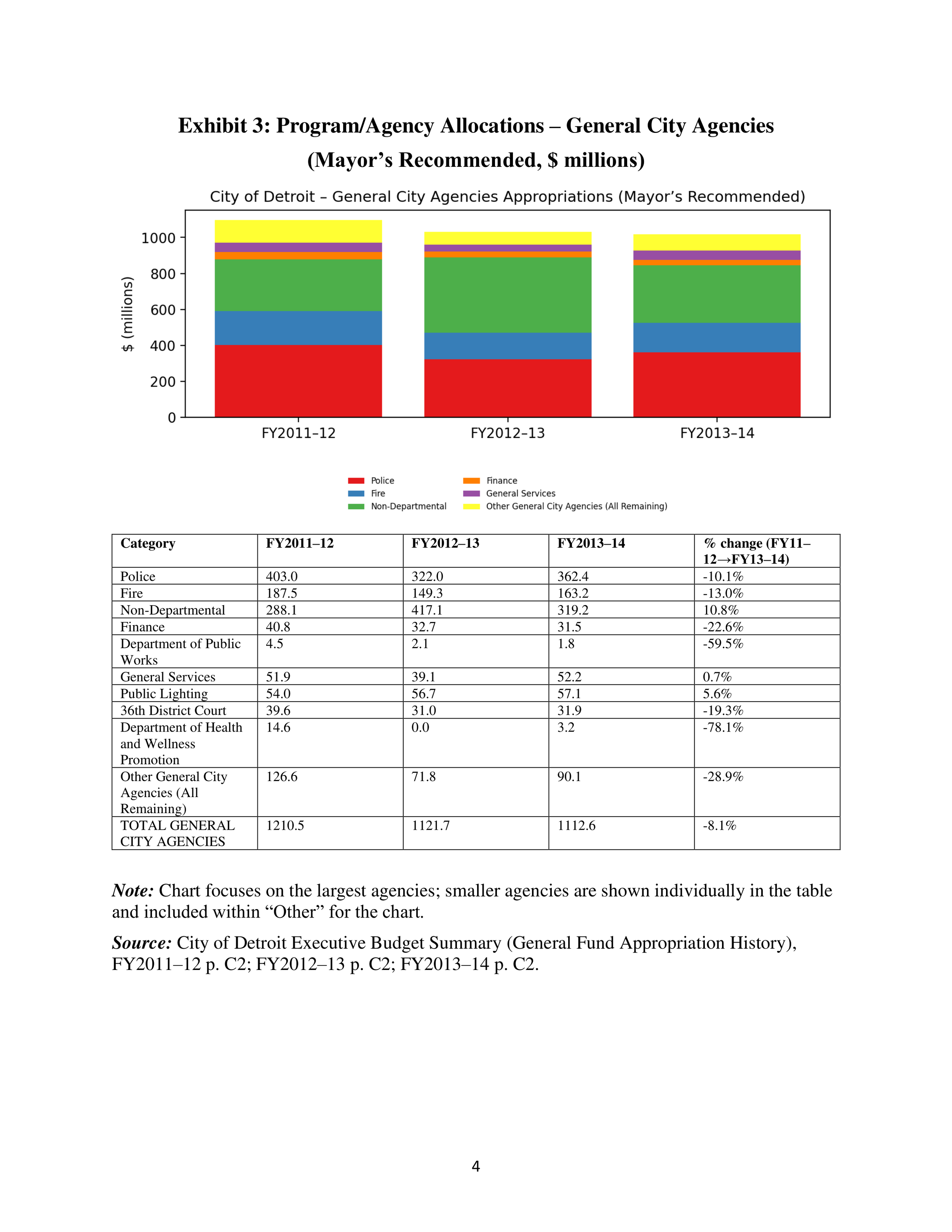

Public Safety Dominance

Police and fire remained the largest agency allocations.

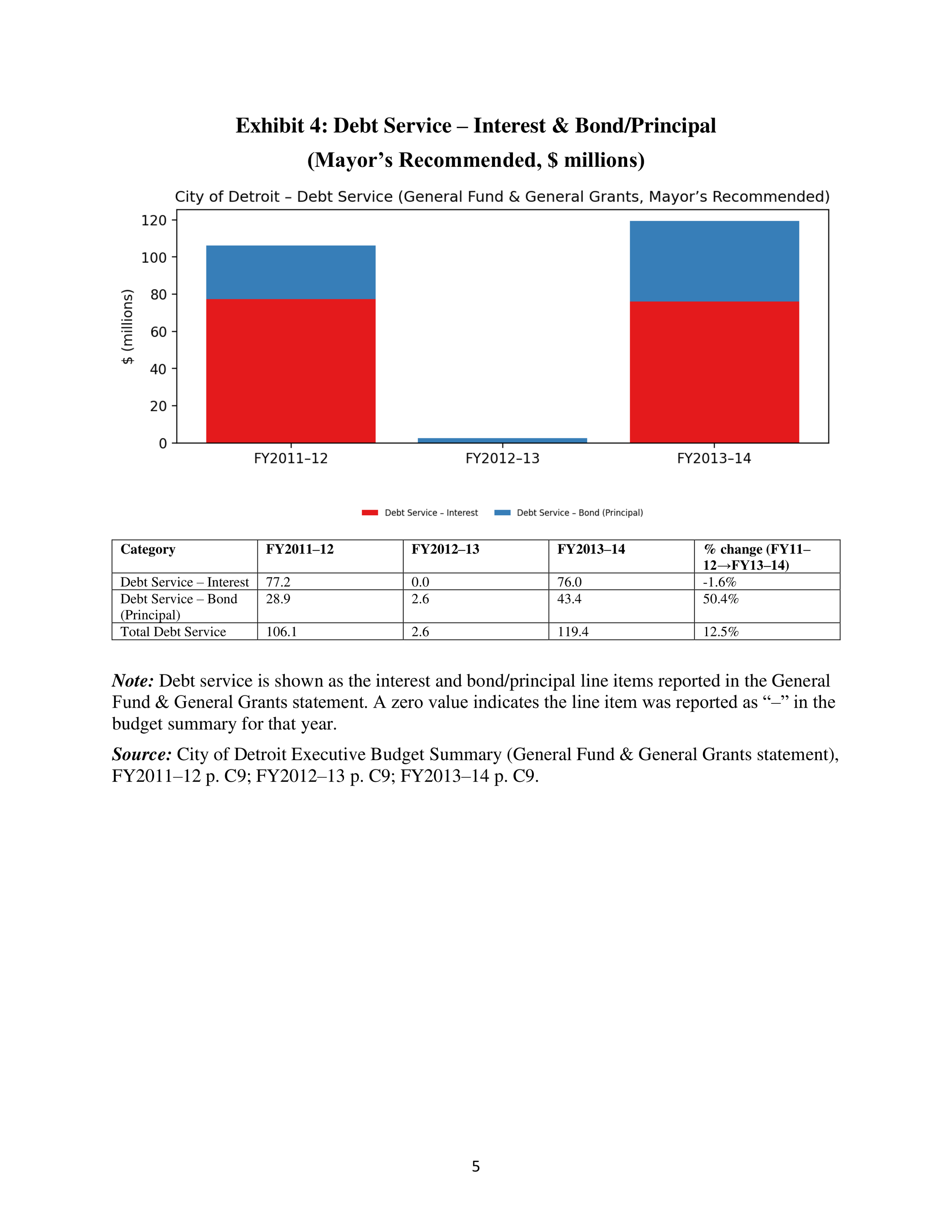

Debt-Service Pressure

Debt service remained a significant claim on General Fund resources.

Transparency Lens Applied

Used the “instrument of democracy” and IMF fiscal-transparency perspective.

Overview

This project examined Detroit’s General Fund budgets in the years leading up to the city’s bankruptcy, using budget documents to analyze revenue capacity, expenditure patterns, debt-service burden, and public transparency. The brief treated the budget not just as a financial record, but as a civic document that should help residents understand fiscal priorities, constraints, and warning signs.

What I Analyzed

The project focused on four core budget questions:

Were Detroit’s revenues stable enough to sustain core services?

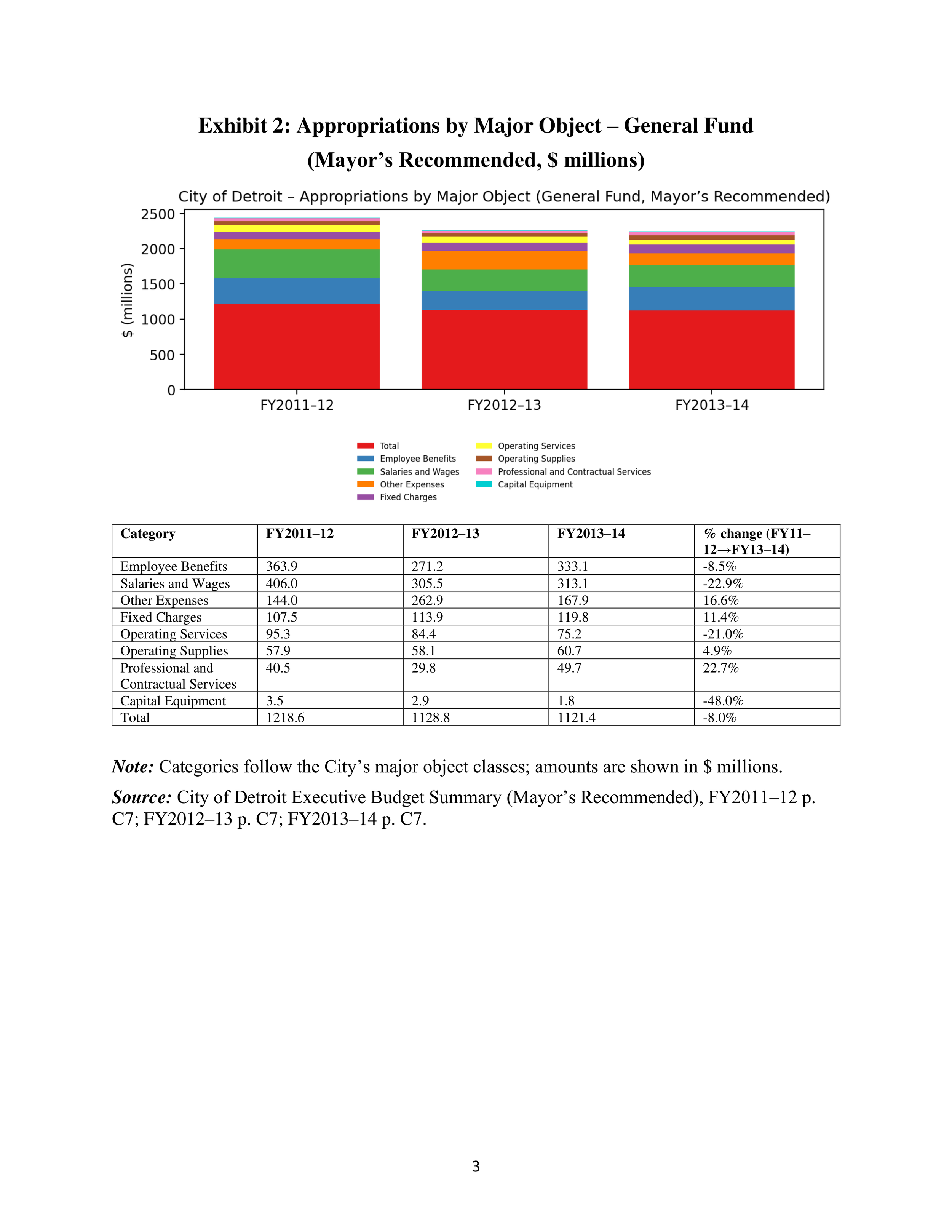

Were expenditures flexible, or dominated by hard-to-reduce costs?

Did agency allocations reveal meaningful shifts in public priorities?

Was debt service presented clearly enough for citizens to understand its fiscal impact?

To answer these questions, the brief compared major revenue sources, object-class expenditures, agency allocations, and debt-service figures across three fiscal years.

Key Fiscal Diagnosis

The analysis concluded that Detroit’s fiscal distress was best understood as the interaction of three forces:

A weakening own-source revenue base,

A rigid expenditure structure with major fixed or politically protected costs,

Continuing debt-service pressure that limited budget flexibility.

This diagnosis showed that the city’s problem was not a one-year imbalance, but a structural condition visible in the pattern of declining revenue, constrained spending choices, and reduced discretionary capacity.

Why Transparency Mattered?

A major contribution of the project was its fiscal-transparency assessment. Using the IMF lens, the brief argued that public budget documents should be comprehensive, clear, comparable, and understandable to non-experts. Detroit’s executive summaries were publicly available and visually accessible at a high level, but changes in classification, multi-fund complexity, and inconsistent treatment of debt-related categories made true year-to-year comparison difficult for ordinary readers.

In that sense, the project asked not only whether Detroit had a fiscal crisis, but whether the city’s public documents made the crisis legible enough for democratic accountability.

Why It Matters?

This project demonstrates the ability to interpret public budgets critically rather than descriptively. It reflects skills in fiscal trend analysis, expenditure interpretation, debt-service reading, transparency assessment, and public-facing budget communication. It also shows an important professional strength: the ability to connect financial data to governance, accountability, and institutional trust.

Professional Relevance

This work is directly relevant to government, oversight, budgeting, and fiscal-policy settings because it shows how budget documents can be used to diagnose structural problems, assess transparency, and communicate public-finance realities more clearly. It bridges technical budget analysis with broader public-management concerns about visibility, comparability, and accountability.

Key Skills

Skills Demonstrated:

Municipal budget analysis

Revenue and expenditure trend interpretation

Debt-service analysis

Fiscal transparency assessment

Public accountability framing

Document-based financial analysis

Professional budget writing

Personal Reflection

This project reflects my graduate training in budgeting and financial management and my interest in how public budgets function not only as fiscal instruments, but also as tools of transparency, accountability, and democratic understanding.

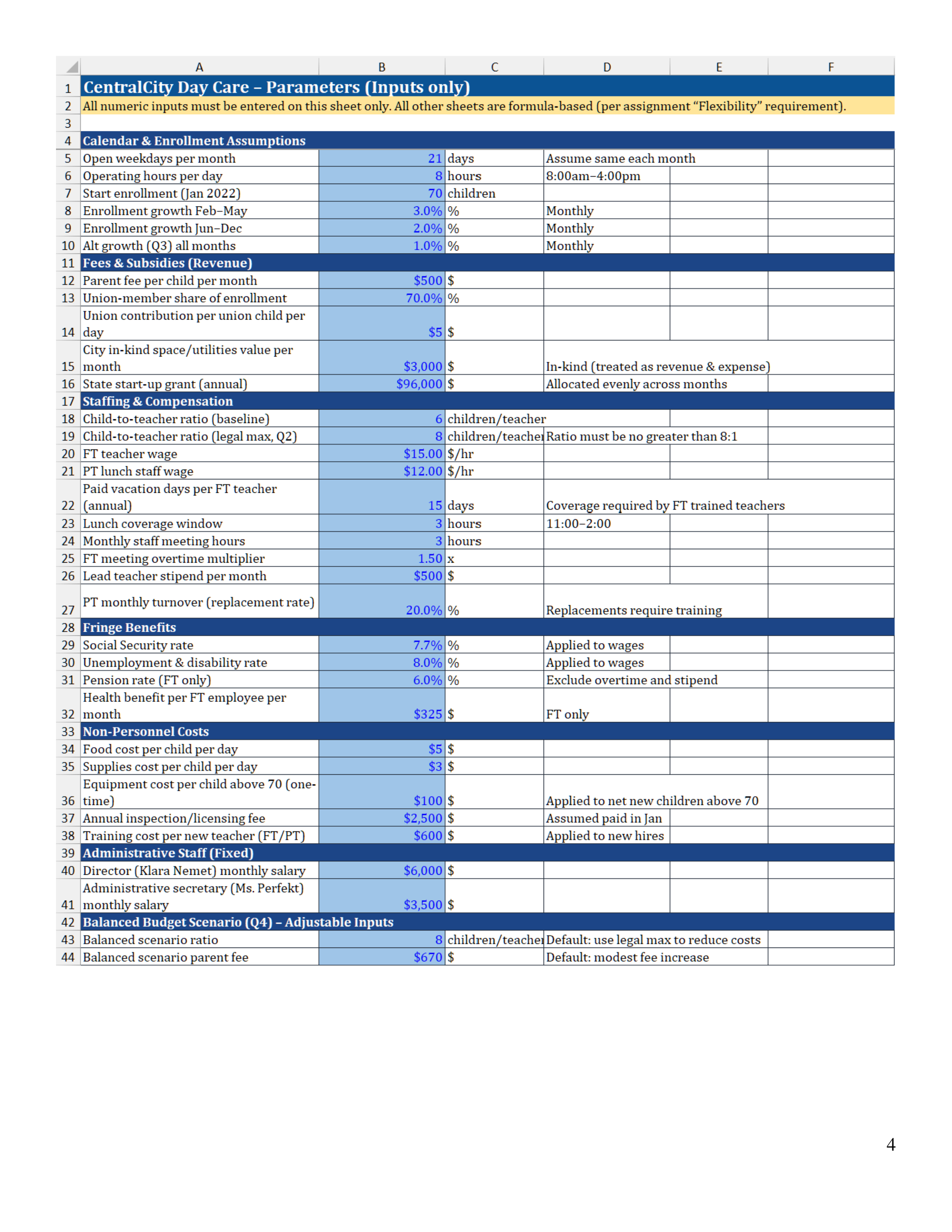

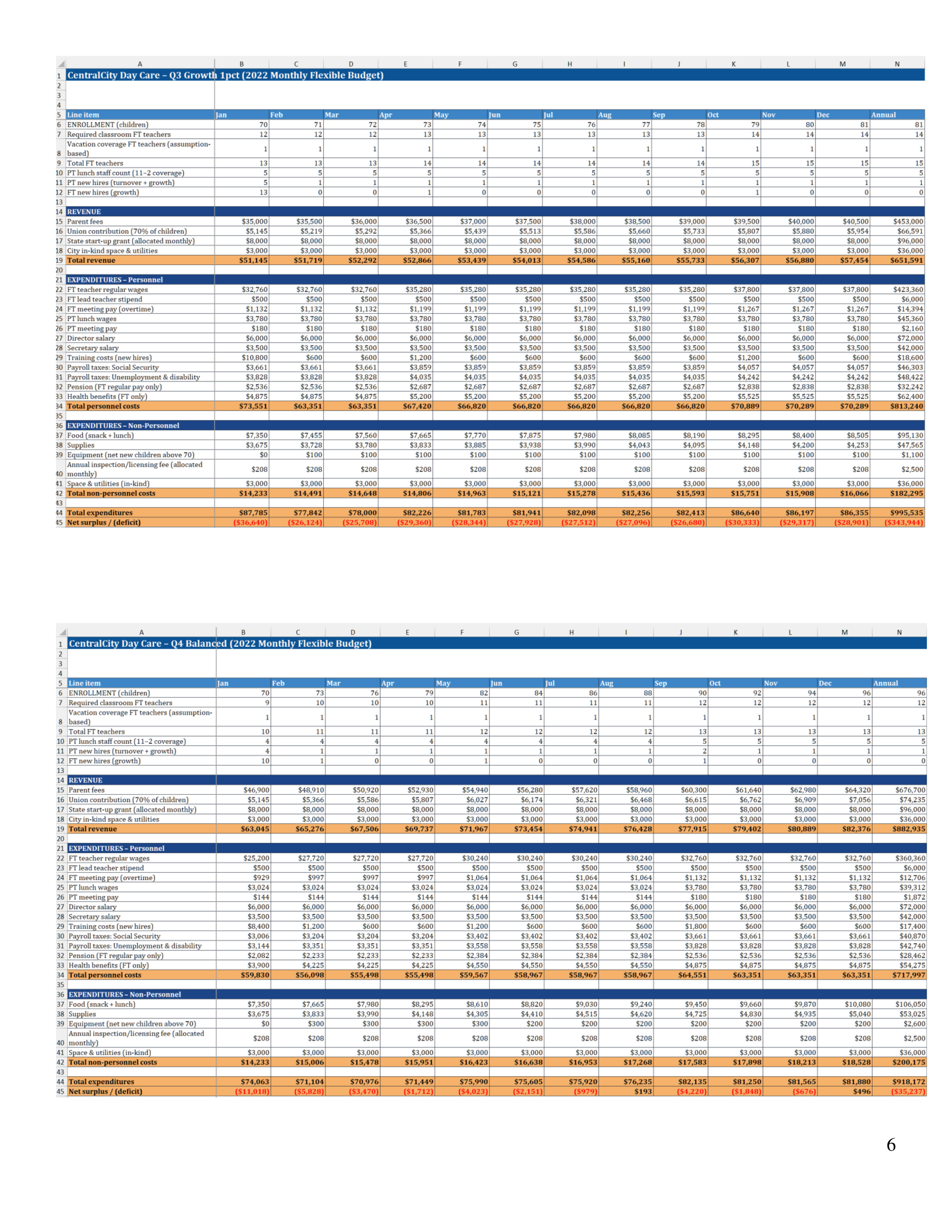

CentralCity Day Care Flexible Budget Brief

Metrics

$335,443 Baseline Deficit

Initial annual gap under baseline assumptions.

82.1% Personnel-Driven Costs

Wages, payroll taxes, and benefits dominated expenditures.

6:1 to 8:1 Ratio Test

Staffing ratio changes had the largest budget impact.

4 Scenario Results Compared

Baseline, legal maximum ratio, 1% growth, and balanced-budget scenario.

$763 Balanced-Budget Surplus

Achieved in the recommended scenario.

Overview

This project developed a flexible, parameter-driven 2022 budget model for a proposed municipal day care center in CentralCity. The analysis focused on a practical public-management problem: how to align revenue assumptions, staffing requirements, and operating costs so the center could remain financially viable while meeting legal requirements and supporting informed policy decisions.

What I Analyzed

The project used a spreadsheet-based flexible budget to test multiple scenarios rather than relying on a single static budget. The model included:

a baseline 2022 budget,

a legal maximum child-to-teacher ratio scenario,

a lower-growth enrollment scenario,

and a balanced-budget scenario.

Note: This structure made it possible to compare how staffing rules, parent fees, and enrollment assumptions affected annual revenues, annual expenditures, and the center’s year-end fiscal position.

Key Budget Diagnosis

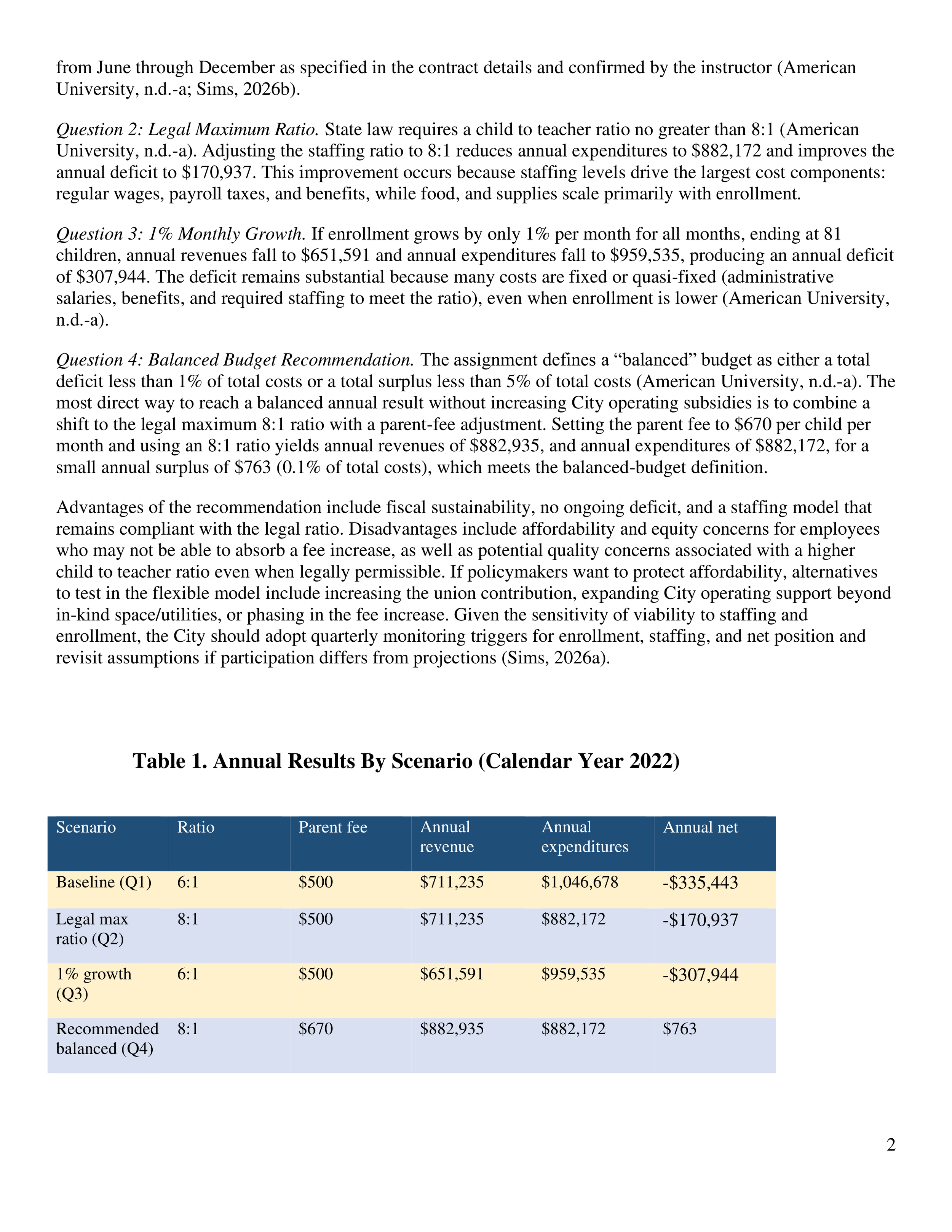

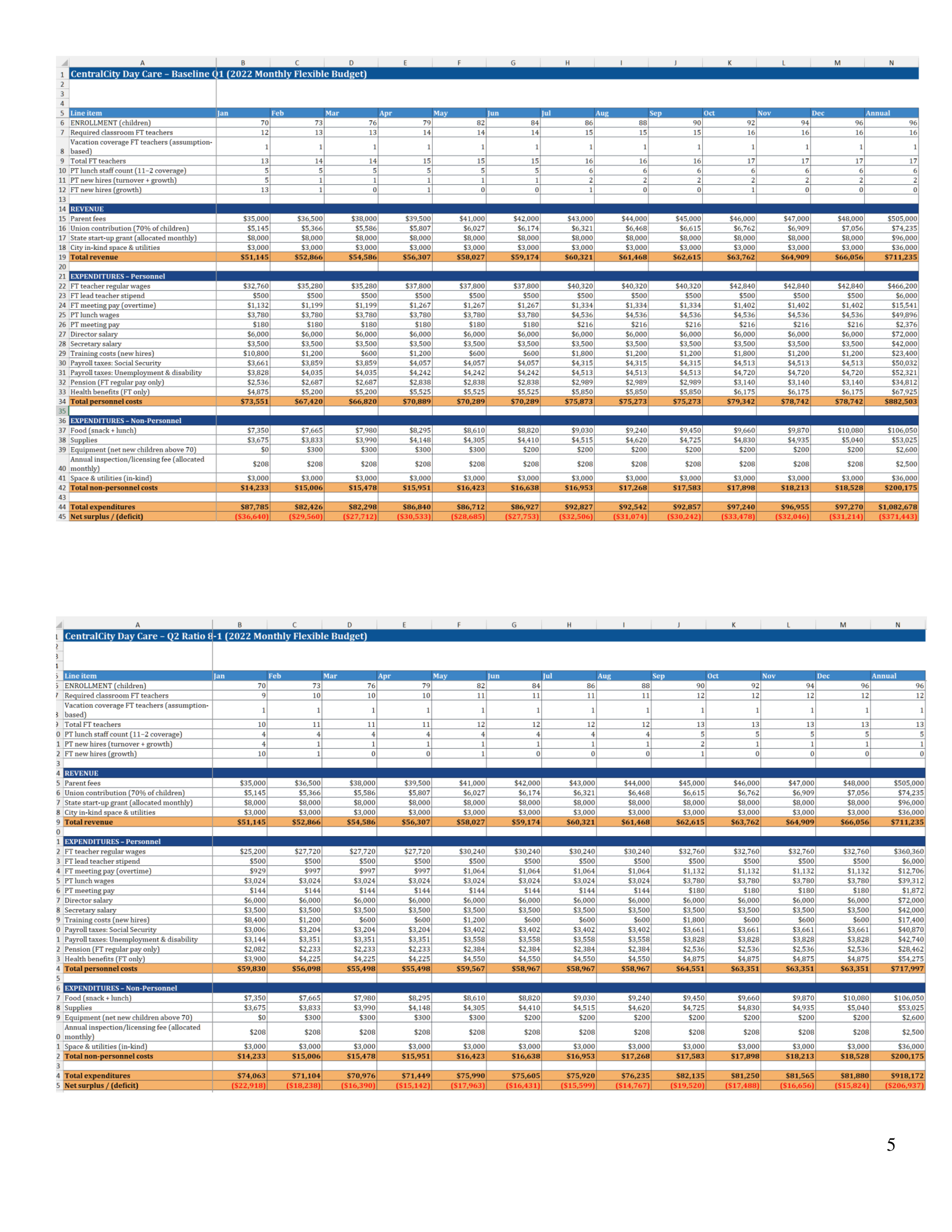

The baseline budget revealed that the center was not financially sustainable under the original assumptions. Annual revenues totaled $711,235, while annual expenditures reached $1,046,678, producing a deficit of $335,443. The largest cost driver was personnel: wages, payroll taxes, and benefits accounted for more than four-fifths of total expenditures. That finding made it clear that staffing assumptions were central to any serious budget solution.

Scenario Analysis

The project showed that changing the staffing ratio from 6:1 to the legal maximum 8:1 substantially improved the budget by reducing annual expenditures to $882,172 and shrinking the deficit to $170,937. A separate 1% monthly-growth scenario lowered both revenues and expenditures, but still left a significant deficit because many costs remained fixed or quasi-fixed even with lower enrollment.

These scenarios demonstrated an important budgeting lesson: some fiscal pressures respond quickly to enrollment changes, while others are driven by structural operating requirements that do not fall proportionally.

Recommendation

The recommended balanced-budget scenario combined two changes:

Adoption of the legally permissible 8:1 child-to-teacher ratio,

Increase in the parent fee from $500 to $670 per month.

Note: Under that package, annual revenues rose to $882,935, annual expenditures were $882,172, and the center produced a small annual surplus of $763, meeting the assignment’s balanced-budget definition.

Trade-Offs & Policy Implications

A key strength of this project is that it did not present fiscal balance as a purely technical outcome. The recommendation also identified meaningful trade-offs. A higher parent fee improved sustainability, but raised affordability and equity concerns for families. A higher child-to-teacher ratio remained legally compliant, but could affect service quality even while improving the budget. The brief, therefore, treated budgeting as a decision-making process that must weigh fiscal sustainability, compliance, affordability, and service outcomes together.

Why It Matters?

This project demonstrates the ability to connect budgeting tools to real management decisions. It reflects skills in flexible budgeting, scenario modeling, cost-structure analysis, revenue design, and public-sector trade-off assessment. It also shows an important managerial strength: the ability to distinguish between what is financially possible, what is legally allowable, and what remains socially or politically sensitive.

Professional Relevance

This work is directly relevant to budgeting, operations, program management, and local government settings because it shows how flexible budgets can support decision-making under uncertainty. It demonstrates that I can identify cost drivers, test policy-relevant assumptions, compare options, and make recommendations that are financially grounded while still attentive to broader implementation and equity concerns.

Key Skills

Skills Demonstrated:

Flexible budgeting

Scenario modeling

Revenue and expenditure analysis

Staffing-ratio cost interpretation

Balanced-budget strategy

Trade-off analysis

Professional budget writing

Personal Reflection

This project reflects my graduate training in budgeting and financial management and my interest in how public institutions can use flexible budgeting to make more realistic, transparent, and policy-aware financial decisions.